Artazum // Shutterstock

How to get equity out of your home without refinancing

U.S. homeowners are sitting on a historic amount of housing wealth. According to Federal Reserve data, homeownersâ equity as a share of real estate value recently approached the highest levels in decades, with total equity estimated at $34.39 trillion nationwide.

That amount of equity creates options for homeowners who want access to cash without refinancing their mortgage. Understanding how these options work can help you decide which approach, if any, fits your situation.

In this guide, Splitero explores the various ways to access your home equity without refinancing and how they work to help you determine which may be right for you.

Key Takeaways

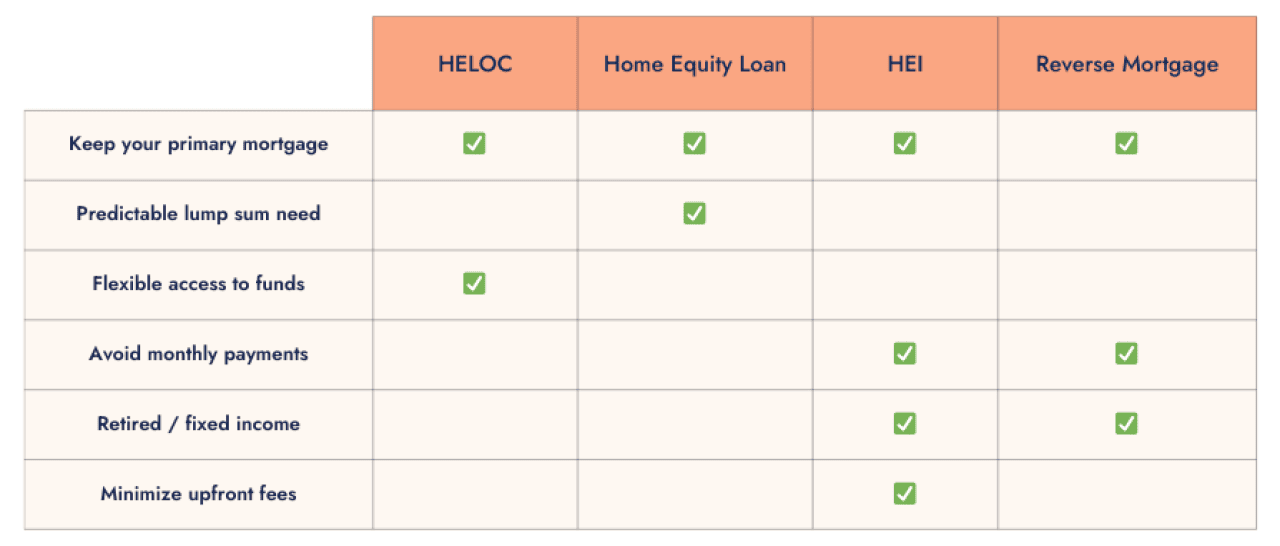

- Refinancing isnât the only path: You can access equity while keeping your existing mortgage intact.

- Match the various options to your goals: Home equity loans suit predictable, one-time cash needs; HELOCs offer flexible access; HEIs and reverse mortgages provide funds without monthly payments.

- Repayment varies: HELOCs shift to principal-and-interest after the draw period, loans start fixed payments immediately, HEIs tie repayment to home value, and reverse mortgages defer until sale or vacancy.

- Check your eligibility: HELOCs and loans require credit and income, HEIs are more flexible, reverse mortgages require homeowner age be 62+.

- Compare costs: Interest, fees, and long-term trade-offs differ depending on your timeline and financial goals.

Can you take equity out of your home without refinancing?

Yes. You can access your homeâs equity through several methods that donât involve refinancing. Home equity is the difference between your homeâs current market value and your outstanding mortgage balance. Depending on your financial situation and goals, you may be able to access up to around 80% of that value through many different methods other than refinancing.

Before choosing an option, think about:

- How much equity you want to access

- Whether monthly payments make sense

- How long you expect to stay in your home

How to pull equity out of your home without refinancing

There are several ways to access your home equity without refinancing your mortgage. These options differ in terms of how much equity you can tap, whether monthly payments are required, and how repayment works over time. Some involve paying interest and taking on traditional debt, while others allow you to unlock cash by sharing a portion of your homeâs future value. Knowing these differences can help you choose the approach that best fits your goals, timeline, and financial situation.

1. Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit secured by your homeâs equity. With a HELOC, homeowners can typically access 80â85% of their homeâs value minus the outstanding mortgage balance. During the draw period, usually 5â10 years, you can borrow, repay, and borrow again as needed while making interest-only payments on the amount used. Once the draw period ends, the remaining balance enters the repayment phase, often lasting 10â20 years, during which monthly payments include both principal and interest.

Requirements/considerations

- Equity threshold: Most lenders require at least 15â20% equity remaining in your home after borrowing.

- Credit and income: Typically, a credit score of 620+ and proof of income are required, with a debt-to-income ratio below 45%.

- Rate structure: HELOCs usually have variable interest rates, meaning monthly payments can rise.

Fees: May include appraisal, origination, and annual maintenance fees.

Pros

- Flexible access: Borrow only what you need and repay to reborrow during the draw period.

- Interest-only option: Reduces initial payments and preserves short-term cash flow.

- Reusable credit: Available credit replenishes as you repay.Â

Cons

- Payment increases after the draw period: Once the draw period ends, remaining balances shift to principal-and-interest payments, which can significantly increase your monthly obligation.

- Variable interest rates: Because rates adjust with the market, your borrowing costs can rise over time, even if your balance stays the same.

- Budget uncertainty: Changing rates and payment structures make long-term budgeting more complex compared to fixed-rate options.

Best for

Homeowners who need flexible access to funds for ongoing or variable expenses. Ideal for projects that come up over time rather than a single planned cost. A HELOC is also useful for those who are comfortable with interest-only payments initially and plan for higher monthly payments later.

How it differs

Unlike a home equity loan, a HELOC is not a fixed lump sum and adapts to ongoing financial needs. HELOCs are revolving lines of credit with a draw period followed by repayment, with interest-only payments during the draw period providing short-term flexibility. After the draw period, principal and interest payments begin, typically over 10â20 years.

2. Home Equity Loan

A home equity loan provides a fixed lump sum based on your available equity, usually up to 80â85% of your homeâs value minus any mortgage balance. Repayment starts immediately with fixed monthly payments that typically continue for a period of 10â30 years, allowing for predictability and a clear total cost.

Requirements/considerations

- Equity threshold: Must maintain at least 15â20% equity after borrowing.

- Credit and income: Generally requires a credit score of 620+ and verifiable income.

- Upfront costs: Closing, appraisal, and origination fees may apply.

- Repayment: Begins immediately with principal and interest.

Pros

- Predictable monthly payments: Fixed interest rates and set repayment terms make it easier to plan and budget over the life of the loan.

- Clear borrowing structure: Receiving a lump sum upfront works well when you know exactly how much cash you need.

- Rate stability: Payments are not affected by market rate changes, which protects against rising interest costs.

Cons

- Limited flexibility: Once the loan is funded, you cannot access additional equity without applying for a new loan.

- Immediate interest accrual: Interest begins accruing on the full loan amount right away, even if you do not use all of the funds immediately.

- Monthly payment obligation: Fixed payments start immediately, which can reduce monthly cash flow.

Best for

Homeowners who want a one-time cash amount with predictable monthly payments. This option works well for planned expenses such as home renovations, medical bills, or consolidating higher-interest debt. Monthly payments start immediately and remain consistent for the life of the loan, making it easier to budget.

How it differs

Home equity loans provide a single lump sum with fixed monthly payments. Unlike HELOCs, you cannot reborrow once funded. Payments are set for the term, giving predictability but no flexibility for future or variable expenses.

3. Home Equity Investment (Shared Equity Agreement)

A home equity investment (HEI) allows homeowners to access cash by partnering with an investor who receives a portion of the homeâs future appreciation. In this arrangement, homeowners can typically access 10â25% of the homeâs current value. Repayment occurs when the home is sold, refinanced, or at the end of the agreement, typically 10â30 years. Monthly payments are not required, but you will ultimately share a portion of the appreciation with the investor.

Requirements/considerations

- Equity threshold: Usually, 15â20% equity or more is required.

- Credit and income: Flexible requirements; some providers accept lower scores (minimum 500) and many providers do not have income requirements.

- Repurchase obligation: Investor share is repaid at sale, refinance, or the end of your term.

- Long-term planning: Total repayment depends on future home value.

Pros

- No monthly payments: Because repayment is deferred, this option preserves monthly cash flow and reduces short-term financial strain.

- Flexible qualifications: Credit score and income requirements are often more accommodating than traditional lending options.

- Use funds on your terms: Cash can be used for a wide range of needs, from home improvements to investing or consolidating obligations.Â

Cons

- Share of future home value: The amount you repay is tied to your homeâs value when you exit the agreement, which means the total cost of accessing your equity depends on how your home performs over time.

- Limited availability: HEIs are not available in every state.

- Limits ability to refinance: If you want to refinance later, your lender may require you to settle your HEI first.

Best for

Homeowners seeking cash today without monthly payments or added debt. This option is especially useful for retirees, self-employed homeowners, or anyone with a variable income who plans to stay in their home long-term. Accessing equity this way preserves monthly cash flow while providing funds for large projects or investments.

How it differs

Your repurchase amount is tied to your homeâs value at sale, refinance, or term-end rather than a fixed monthly schedule. You receive cash upfront while sharing a portion of future appreciation with the investor. This approach prioritizes flexibility and keeps short-term finances unaffected.

4. Reverse Mortgage (for eligible homeowners)

A reverse mortgage lets homeowners 62+ convert home equity into cash while deferring monthly payments. Homeowners can access 50â60% of their homeâs value depending on their age, interest rates, and existing mortgage balance. Funds can be received as a lump sum, a line of credit, or monthly distributions. Repayment occurs when the home is sold, the homeowner moves out, or the property is no longer the ownerâs primary residence.

Requirements/considerations

- Age requirement: At least one borrower must be 62+.

- Primary residence: Must live in the home during the entire financing term.

- Equity threshold: Home should be mostly or fully paid off.

Pros

- No required monthly mortgage payments: This helps retirees maintain cash flow while continuing to live in their home.

- Multiple payout options: Homeowners can choose a lump sum, line of credit, or monthly payments based on their needs.

- Age-based qualification: Eligibility is driven primarily by age and equity rather than income or credit score.Â

Cons

- Growing loan balance: Interest accrues over time, increasing the total amount owed when the loan becomes due.

- Higher upfront costs: Origination fees, closing costs, and mortgage insurance can be more expensive than other equity options.

- Reduced estate value: Remaining equity available to heirs may be lower after repayment.

Best for

Homeowners 62+ who want access to equity without monthly payments. Ideal for supplementing retirement income, funding home improvements, or covering other large expenses. Allows older homeowners to unlock significant equity while continuing to live in their home. Borrowing limits depend on the homeownerâs age, interest rates, and remaining equity.

How it differs

Repayment is deferred until the home is sold, vacated, or no longer the primary residence. Monthly mortgage payments are not required, though taxes, insurance, and maintenance must continue. Available funds are generally 50â60% of the homeâs value, with eligibility based on age rather than income or credit.

Is accessing equity without refinancing right for you?

Deciding whether and how to access your home equity depends on your goals, lifestyle, and financial situation. Here are key factors to consider:

1. Your financial goals

- Predictable, one-time expenses: If you have a specific project in mind, like a home renovation or debt consolidation, a home equity loan may be a good fit, as it offers a lump sum with fixed monthly payments.

- Variable or ongoing needs: If you need flexibility to borrow and repay over time, a HELOC could work better.

- Avoiding monthly payments: If you prefer not to add monthly debt obligations, a home equity investment (HEI) or reverse mortgage (if eligible) may make sense.

2. Your timeline

How long you plan to stay in your home matters. Short-term homeowners may not benefit from long-term options like a reverse mortgage or HEI, while long-term homeowners may maximize flexibility and minimize costs by choosing them.

3. Your comfort with risk and debt

- HELOCs and home equity loans are debt-based and require repayment with interest, potentially increasing monthly obligations.

- HEIs are non-debt options, but youâll share a portion of your homeâs future value.

- Reverse mortgages allow access without monthly payments, but can reduce inheritance for heirs and carry higher fees.

4. Eligibility and financial qualifications

- Credit score: Higher credit scores generally mean better HELOC or home equity loan rates. Lower scores may make HEIs easier to qualify for.

- Age: Reverse mortgages are only available to homeowners 62 and older.

- Income and employment status: HELOCs usually require proof of income; HEIs may be accessible even if retired, self-employed, or on a fixed income.

5. Costs and fees

Every option comes with upfront fees (e.g., appraisal, origination, closing costs). Compare these costs against long-term interest or equity sharing to see which aligns best with your goals.

Splitero

Next steps: Always weigh the trade-offs carefully and consider consulting a financial advisor. The right choice depends on your unique financial situation, timeline, and comfort with risk.

Leveraging your home equity doesnât have to mean replacing your mortgage or sacrificing your low rate. An HEI offers homeowners who want to preserve their current mortgage an option to access their equity with no added monthly payments.

Frequently Asked Questions

How much equity can you access without refinancing?

Most options allow homeowners to access a portion of their total equity, typically up to around 80% of the homeâs value minus existing debt, depending on credit and lender criteria.

Whatâs the difference between a HELOC and a home equity loan?

A HELOC provides a flexible credit line you can reuse and draw from; a home equity loan gives a single fixed lump sum with fixed monthly payments.

Will taking out a second mortgage affect selling your home later?

Yes. When selling, any liens, including second mortgages, must be paid off before proceeds are distributed.

How do shared equity agreements work when you sell or refinance?

You repurchase your investment option when selling or refinancing based on your agreementâs terms, reflecting your homeâs value at that time.

This story was produced by Splitero and reviewed and distributed by Stacker.

![]()